Cheap Rent Can Breach Pay

The Accommodation Offset: Getting Staff Housing Right for NMW

A pub company charges its live-in manager £120 a week for the flat above the bar. The flat is worth twice that on the open market. The manager earns £12.71 an hour. On paper, everything looks fine. Then HMRC calculates the effective hourly rate, and the company ends up on the naming list.

The accommodation offset is the only benefit-in-kind that counts towards the National Minimum Wage. Not meals, not a company car, not childcare vouchers: only accommodation. And the rules around it are strict enough that 31 employers in a single naming round got the offset calculation wrong. Major hospitality brands, including Shepherd Neame, Mitchells & Butlers, and City Pub Group, have been publicly named for underpaying the minimum wage.

The offset rate

From April 2026, the accommodation offset is £11.10 per day (£77.70 per week).

That figure is a cap, not a target. It sets the maximum amount an employer can charge for accommodation before it starts eating into a worker's pay for NMW purposes.

Previous rates for reference:

| Year | Daily rate | Weekly rate |

|---|---|---|

| 2026 | £11.10 | £77.70 |

| 2025 | £10.66 | £74.62 |

| 2024 | £9.99 | £69.93 |

The rate changes every April. The new figure is announced ahead of the effective date (the April 2026 rates followed Low Pay Commission advice published in November 2025), which leaves a window to check current accommodation charges against the new cap before it takes effect.

How the calculation works

Three scenarios.

Charge below the offset. A hotel charges kitchen staff £60 a week for a shared house. The offset is £77.70. The charge is below the cap, so there is no impact on NMW calculations. The worker's pay stands as it is.

Charge above the offset. A pub charges its live-in manager £120 a week. The offset is £77.70. The difference, £42.30, is treated as a deduction from pay for NMW purposes. If that deduction pushes the manager's effective hourly rate below £12.71, there is a breach. It does not matter that £120 a week is below market rent for the area. The offset is the offset.

Accommodation provided free. The full offset, £77.70 per week, is added to the worker's pay for NMW purposes. Free accommodation works in the employer's favour.

Under the NMW Regulations, the charge includes everything connected to the accommodation: rent, utilities, furniture, laundry. A charge of £77.70 for the room with a separate £30 for electricity on top would be treated as a single accommodation charge of £107.70 and measured against the offset in full.

The pub and hotel trap

Live-in arrangements are common across hospitality. Pub managers in tied accommodation. Hotel workers in staff housing. Seasonal staff in rooms above the restaurant. Every one of these is exposed to the same calculation.

The trap is market thinking. A landlord looks at the flat above the pub and thinks: this would let for £800 a month on the open market. Charging £500 feels generous. But £500 a month is roughly £115 a week. That is £37.30 above the offset. For a manager working 45 hours a week at £12.71 an hour, that £37.30 weekly deduction drops their effective rate to about £11.88, below the NMW floor. A breach.

The correct test is to work backwards from the worker's hourly rate, subtract the excess accommodation charge spread across their hours, and confirm the result still clears £12.71.

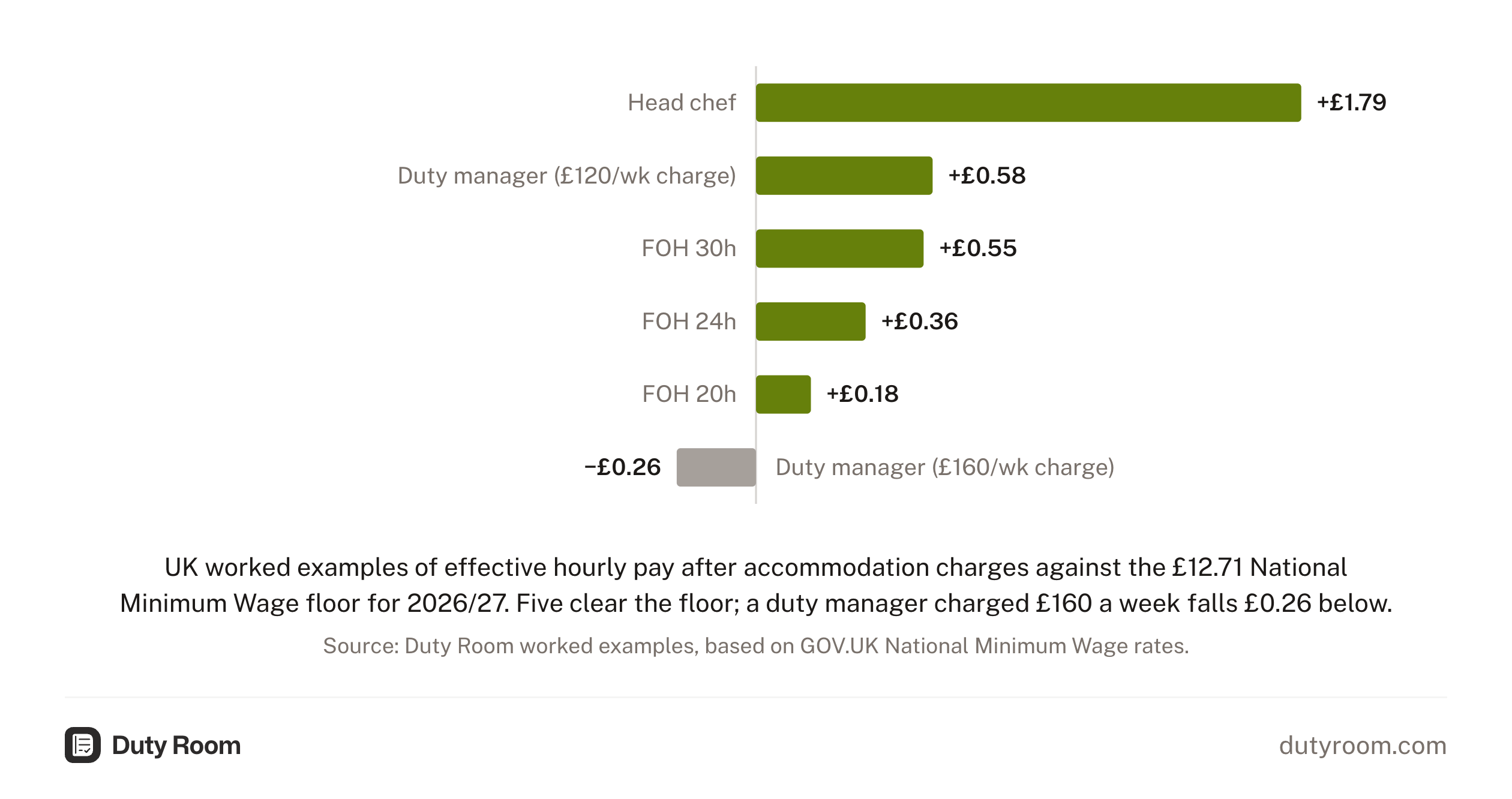

Worked examples at April 2026 rates:

| Role | Weekly hours | Weekly gross pay | Accommodation charge | Excess over offset | Effective hourly rate | Compliant? |

|---|---|---|---|---|---|---|

| Head chef | 40 | £580.00 | £77.70 | £0.00 | £14.50 | Yes |

| Duty manager | 48 | £680.00 | £120.00 | £42.30 | £13.29 | Yes |

| Duty manager | 48 | £680.00 | £160.00 | £82.30 | £12.45 | No |

| FOH (variable) | 30 | £420.00 | £100.00 | £22.30 | £13.26 | Yes |

| FOH (variable) | 24 | £336.00 | £100.00 | £22.30 | £13.07 | Yes |

| FOH (variable) | 20 | £280.00 | £100.00 | £22.30 | £12.89 | Yes |

{kind=link}

| Role | Weekly hours | Accommodation charge | Effective hourly rate | Compliant? |

|---|---|---|---|---|

| Head chef | 40 | £77.70 | £14.50 | Yes |

| Duty manager | 48 | £120.00 | £13.29 | Yes |

| Duty manager | 48 | £160.00 | £12.45 | No |

| FOH (variable) | 30 | £100.00 | £13.26 | Yes |

| FOH (variable) | 24 | £100.00 | £13.07 | Yes |

| FOH (variable) | 20 | £100.00 | £12.89 | Yes |

The FOH rows illustrate the variable-hours exposure: the same £100 weekly charge is compliant at 24 hours and becomes non-compliant once weekly hours drop to around 17. A minimum-hours floor of 20 leaves a buffer of nearly three hours at that charge level.

Calculate it per pay reference period

The offset is calculated per pay reference period, not annually. A monthly-paid manager has a monthly pay reference period. A weekly-paid kitchen porter has a weekly one.

If hours vary between periods (and in hospitality, they often do), the same accommodation charge can be compliant in a busy month and non-compliant in a quiet one. Fewer hours means the accommodation deduction has a larger per-hour impact.

A manager who works 50 hours a week during December and 35 hours a week in January pays the same rent both months. The NMW impact is different in each period. Operators with variable-hours live-in staff typically model both the busiest and quietest expected periods before confirming a charge.

Records

The NMW Regulations require employers to keep records sufficient to show that the minimum wage has been paid for every pay reference period where accommodation is provided. The records that show this in practice are:

- The accommodation charge, broken down if it includes utilities or other costs

- The offset rate applied (which changes annually)

- Hours worked in each pay reference period

- The resulting effective hourly rate after the offset calculation

The civil recovery period for NMW underpayment claims is six years, and records must be kept for that period. From 7 April 2026, legal responsibility for NMW enforcement sits with the Fair Work Agency, with HMRC running NMW casework on its behalf under contract until the full transfer in April 2027. The record-keeping obligation is unchanged.

Where records are absent, the practical burden of showing the wage was paid sits with the employer.

Correcting historical shortfalls

Operators who identify a past underpayment typically calculate the arrears for each affected pay reference period, working back to the point the charge or the hours first created a shortfall. They then top up the worker's next pay packet for that full amount, noting the correction in the payroll file. The six-year civil recovery window means the scope of any correction exercise runs back that far at maximum, though the practical starting point is usually the last April rate change that went un-modelled. Where the breach spans multiple workers or multiple rate years, operators commonly produce a schedule listing each period, the shortfall per period, and the gross arrears figure, which then forms part of the payroll record. The Fair Work Agency's published enforcement policy treats the two situations differently: an operator who has repaid the arrears and documented the correction before an investigation starts is in a materially better position than one whose shortfall is found by investigators.

Getting it right

The accommodation offset is the only benefit-in-kind that counts towards NMW. Everything else an employer provides, from staff meals to transport, sits outside the NMW calculation entirely.

For operators running the annual cycle, practice converges on four steps:

- When the revised offset rate is announced, review current accommodation charges against the new cap before the April effective date.

- Model the effective hourly rate for every worker in live-in accommodation across the range of expected hours. Include their quietest anticipated pay reference period, not just a typical one.

- Document the arrangement in writing: what is provided, what is charged, and which offset rate was applied.

- Notify affected workers of any change to their accommodation charge before the new rate takes effect.

The error the offset invites is mechanical: the rate changes in April, the charge does not, and the shortfall compounds across pay reference periods until someone checks. The six-year civil recovery window means a missed April update can generate arrears claims stretching back to 2020.

For the full picture on NMW traps in hospitality, including uniforms, unpaid training, clock-rounding, and tips, see our employment records resources.

This briefing is based on sources available at publication and is for general information only. It doesn't constitute legal advice. For advice on your specific situation, consult a qualified professional.

Produce the record when you're asked, not a week later.

Duty Room helps operators and their HR adviser stay aligned on right-to-work checks, working time records, tipping allocations, and policy renewals across each site.